Page 8 - KPMG Tax in Romania

P. 8

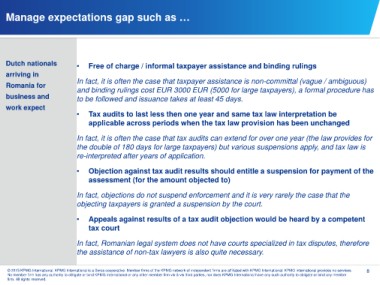

Manage expectations gap such as …

Dutch nationals • Free of charge / informal taxpayer assistance and binding rulings

arriving in

Romania for In fact, it is often the case that taxpayer assistance is non-committal (vague / ambiguous)

business and and binding rulings cost EUR 3000 EUR (5000 for large taxpayers), a formal procedure has

work expect to be followed and issuance takes at least 45 days.

• Tax audits to last less then one year and same tax law interpretation be

applicable across periods when the tax law provision has been unchanged

In fact, it is often the case that tax audits can extend for over one year (the law provides for

the double of 180 days for large taxpayers) but various suspensions apply, and tax law is

re-interpreted after years of application.

• Objection against tax audit results should entitle a suspension for payment of the

assessment (for the amount objected to)

In fact, objections do not suspend enforcement and it is very rarely the case that the

objecting taxpayers is granted a suspension by the court.

• Appeals against results of a tax audit objection would be heard by a competent

tax court

In fact, Romanian legal system does not have courts specialized in tax disputes, therefore

the assistance of non-tax lawyers is also quite necessary.

© 2015 KPMG International. KPMG International is a Swiss cooperative. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG international provides no services. 8

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member

firm. All rights reserved.